What Is Florida HOA Reserve Fund Accounting?

Florida community associations carry significant financial obligations that extend beyond day-to-day operating expenses. Florida hoa reserve fund accounting governs how associations set aside money for major repairs and replacements over time.

Chapter 720 of the Florida Statutes requires homeowners associations to maintain reserve accounts for specific components. Proper reserve accounting protects every owner from unexpected special assessments. Therefore, boards must understand how reserve funds work and how to account for them correctly.

Defining Florida HOA Reserve Fund Accounting

Reserve fund accounting refers to the process of setting aside, tracking, and reporting funds designated for future capital expenditures. These funds remain separate from operating accounts at all times. Furthermore, they exist specifically to cover the eventual replacement or major repair of common area components.

This requirement applies to components with a remaining useful life of fewer than thirty years under Chapter 720. Roofs, pavement, pools, and painting typically fall into this category. Consequently, associations must calculate required contributions annually based on component cost and remaining useful life.

Statutory Requirements Governing Reserve Funds

Section 720.303 of the Florida Statutes establishes specific reserve requirements for homeowners associations. Associations must maintain reserve accounts unless the membership votes to waive or reduce reserves through a specific statutory process. Therefore, boards cannot simply choose to skip reserve contributions without proper membership authorization.

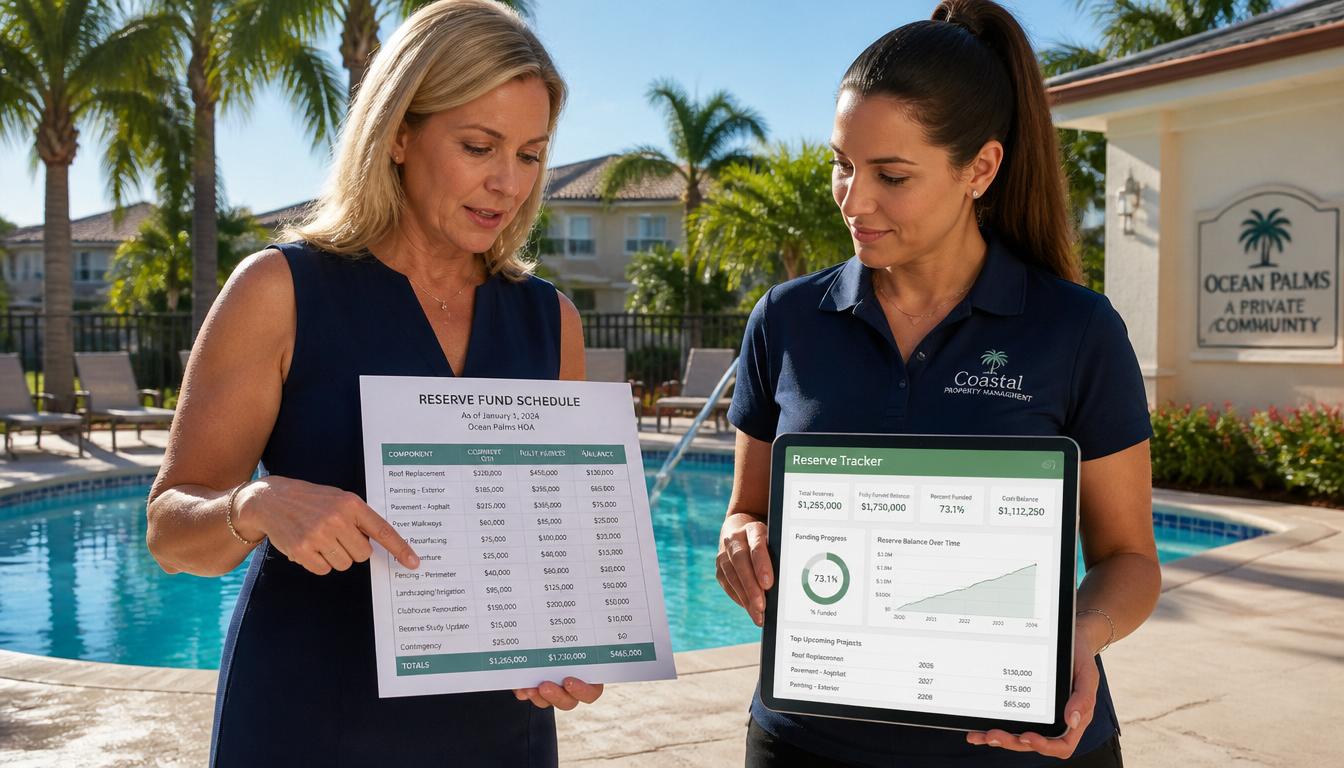

Additionally, Florida law requires associations to include reserve schedules in their annual budgets. These schedules must identify each reserve component, its estimated replacement cost, and the current funding level. Boards that fail to include proper reserve disclosures face statutory compliance exposure.

Two Primary Methods in Florida HOA Reserve Fund Accounting

Two primary funding methods exist within florida hoa reserve fund accounting. The fully funded method aims to accumulate reserves equal to the percentage of each component’s useful life already consumed. The threshold method targets a minimum reserve balance that prevents the fund from falling below a defined floor.

Each method carries different financial implications for owners and the association. Furthermore, neither method eliminates the board’s obligation to calculate and disclose reserve requirements annually. Boards should consult with reserve study professionals when selecting or changing their funding methodology.

Waiving Reserves and Its Financial Consequences

Owners may vote to waive or reduce reserve contributions in any given year under Florida law. However, this decision carries significant long-term financial risk for the community. Consequently, associations that repeatedly waive reserves often face large special assessments when major components reach the end of their useful life.

Boards carry a fiduciary duty to educate owners about the consequences of waiving reserves before any such vote occurs. Presenting clear reserve fund data helps owners make informed decisions. Moreover, accurate reserve accounting makes that educational process far more effective and credible.

Separation of Reserve and Operating Funds

Statutory requirements demand that associations keep reserve funds separate from operating funds at all times. Commingling these funds creates statutory violations and audit findings. Therefore, associations must maintain separate bank accounts for reserve and operating money.

Any transfers between reserve and operating accounts require proper authorization and documentation. Any board member or manager who commingles these funds exposes the association to legal liability. Above all, clear accounting records must reflect every reserve transaction separately and completely.

How Technology Supports Reserve Fund Accounting

Purpose-built software significantly improves how associations manage florida hoa reserve fund accounting. Automated reserve tracking calculates required contributions based on component data entered into the system. Furthermore, integrated reporting generates reserve schedules that satisfy statutory disclosure requirements automatically.

Real-time visibility into reserve balances helps boards make informed decisions throughout the year. They can see exactly how funded each component is at any given moment. Moreover, digital records of every reserve transaction create the audit trail associations need during financial reviews.

Steps for Achieving Goal

- Identify every reserve component on the association’s property and document its estimated replacement cost and remaining useful life.

- Calculate required annual reserve contributions for each component using either the fully funded or threshold funding method.

- Maintain separate bank accounts for reserve and operating funds to prevent commingling and statutory violations.

- Include a complete reserve schedule in the annual budget showing each component, estimated cost, and current funding level.

- Educate owners about the financial consequences of waiving reserves before any membership vote on the topic.

- Adopt purpose-built software that tracks reserve balances and generates statutory reserve disclosures automatically.

- Review reserve fund balances at every board meeting and compare current levels against the reserve study schedule.

Key Takeaways

- Florida hoa reserve fund accounting governs how associations set aside money for future capital expenditures.

- Chapter 720 requires associations to maintain reserve accounts for components with fewer than thirty years of remaining useful life.

- Reserve funds must remain separate from operating funds at all times under Florida statutory requirements.

- Associations may waive reserves through a membership vote, but repeated waivers increase special assessment risk significantly.

- Two primary funding methods exist: fully funded and threshold, each with different financial implications for the community.

- Purpose-built software automates reserve tracking, contribution calculations, and statutory schedule generation for the association.

- Accurate reserve fund accounting supports informed owner decision making and protects the community from financial surprises.

Conclusion

Every Florida community association depends on accurate florida hoa reserve fund accounting to protect its long-term financial health. Boards that manage reserves responsibly reduce the risk of special assessments and maintain stronger property values.

Strong reserve accounting does more than satisfy statutory requirements. Above all, it demonstrates the board’s commitment to protecting every owner’s investment in the community. Therefore, associations that invest in disciplined reserve fund accounting position themselves for long-term financial stability and statutory confidence.

The information provided on this website is NOT to be considered legal advice. Associations and unit owners should consult with legal counsel for the specific application of the Association’s governing documents and Florida Statutes.

{kind=link}